Proposals would rip away assist for center class.

The Republican Examine Committee (RSC) has simply launched its FY 2024 Funds Defending America’s Financial Safety and as soon as once more known as for important cuts to Social Safety. The RSC has served because the conservative caucus of Home Republicans since its founding in 1973, and it at the moment consists of 175 of the 222 Republican Home members. The group has been proposing cuts for many years, however the present spherical places them at odds with the GOP presidential frontrunners. Donald Trump has urged Republicans to not reduce a single penny from Social Safety and Medicare; equally, Ron DeSantis has mentioned that he’s “not going to mess with Social Safety.”

The proposal within the RSC doc is titled Stopping Biden’s Cuts to Social Safety. In case you haven’t heard of any cuts proposed by President Biden, that’s as a result of he hasn’t made any. The provocative title refers back to the cuts that will happen within the early 2030s when the reserves within the belief fund are exhausted. By regulation, Social Safety can not present advantages for which it doesn’t have financing and – as soon as the belief fund is exhausted – incoming payroll taxes and different revenues can be adequate to pay solely 77 p.c of scheduled retirement advantages. Therefore, present and future beneficiaries would see an across-the-board reduce of 23 p.c in 2033.

The exhaustion of the belief fund is certainly an action-forcing occasion. Nobody desires to see advantages instantly reduce by 23 p.c. The choices are simple. Social Safety is an easy system – cash in/cash out. Both more cash should go in or much less cash should exit.

On the money-in facet, the RSC factors out that Biden’s prohibition in opposition to elevating taxes on these incomes beneath $400,000 precludes growing the payroll tax charge. I hope that isn’t a binding constraint; a small improve within the payroll tax charge ought to most likely be a part of any answer. The RSC additionally guidelines out normal revenues by framing such a contribution as coming from borrowing. Certainly, an economically sound strategy would require elevating revenue taxes to generate the required normal revenues. And a powerful rationale exists for a normal income contribution – specifically the price related to having given away the belief discover to early teams of retirees. Particularly, at this time’s employees should contribute rather more to Social Safety than they might to a funded retirement program.

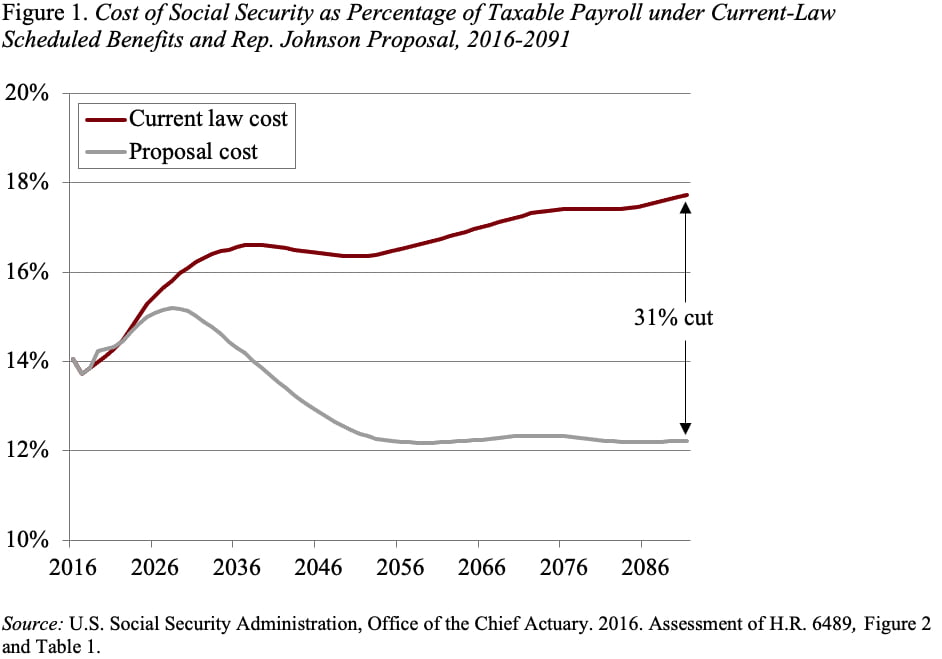

With revenues off the desk, the RSC proposes to eradicate Social Safety’s 75-year deficit solely by reducing advantages. To the extent the that the present bundle, like final 12 months’s, is modelled on a invoice put ahead in 2016 by Sam Johnson (R-TX), it’s price taking a better have a look at that invoice. In response to scoring by the Social Safety actuaries on the time, the Johnson plan would scale back Social Safety prices on the finish of the 75-year projection interval by 31 p.c (see Determine 1).

This 31-percent reduce is the results of three main adjustments:

- elevating the Full Retirement Age – at the moment 67 – to 69;

- dramatically lowering advantages for above-average earners; and

- eliminating the cost-of-living adjustment (COLA) for these with greater incomes and utilizing a chain-weighted inflation index for individuals who qualify for a COLA.

At first look, one may conclude that’s a positive consequence – reduce the advantages of the nicely paid and protect the advantages of the low paid. However the medium employee, who sees advantages drop to 77 p.c of present regulation, had profession common earnings of $58,700 in 2022 and the “excessive” earner, who sees advantages drop to 40 p.c of present regulation, earned $94,000. These aren’t wealthy individuals.

Furthermore, adjustments to Social Safety should be made within the context of your complete retirement revenue system. Many households are more likely to retire with little apart from Social Safety advantages, since at any second in time lower than half the non-public sector workforce participates in an employer-sponsored retirement plan. Policymakers do want to deal with Social Safety’s long-run deficit, however the truth that a majority of Home Republicans might assist a plan that cuts Social Safety by a 3rd ought to terrify voters. Why put out such a doc?

The Entrepreneurial Mindset: Traits to Construct Success

The Entrepreneurial Mindset: Traits to Construct Success{kind=link}