{kind=link}

Viktor utilized FIRE ideas often espoused on this weblog. He grew up an immigrant raised by a single mom on welfare. He retired in 2020 on the ripe previous age of 35. His spouse lately joined him in early retirement.

He is aware of that these ideas have labored for his family. But there’s a sentiment that the FIRE motion was a product of luck. We’ve skilled a simultaneous decade plus bull market in shares, bonds, and actual property accompanied by the introduction of cryptocurrencies for the reason that nice monetary disaster. Constructing wealth was simple.

Was the flexibility to realize monetary independence only a matter of being in the proper place on the proper time? Did folks like Viktor and myself attain the highest of the ladder and pull it up behind us?

In todays’ visitor publish, Viktor shares his private story. He then examines whether or not one thing related is feasible for somebody beginning at zero right now. Take it away Viktor….

Is FIRE Too Good To Be True?

One thing fascinating is going on proper now. On the one hand, you could have a document variety of Gen Zers figuring out or expressing curiosity in retiring early. In actual fact, greater than half of Gen Z respondents take into account themselves a part of the FIRE motion, in response to a latest Credit score Karma survey.

On the similar time, you could have an unprecedented quantity of pessimism about their potential to retire early. Prospects of a decade of low or unfavourable actual financial progress, housing unaffordability, lack of constant residing wages, inflation, faculty debt burdens, bankrupting well being care prices and normal incapacity to avoid wasting… simply to call just a few.

I’m simply getting some stable footing on the opposite aspect of the early retirement journey. I used to be curious whether or not I may need simply squeezed via a door that has successfully closed for the general public at giant.

I wish to discover what the outlook is for somebody beginning right now with zero. How a lot would you could accumulate to succeed in early retirement?

My Journey

I began my skilled profession at Lehman Brothers in the summertime of 2007. Having interned there the earlier summer season, it was a job I completely beloved, discovered intellectually stimulating and financially rewarding.

However inside just a few years, I used to be on my strategy to the ER in the midst of the evening with what I believed was a coronary heart assault. Happily, it turned out to be a panic assault.

My early years on Wall Avenue had been filled with unprecedented upheaval and nice monetary misery because the Nice Recession reared its ugly head. Many individuals misplaced their life financial savings and all hope of offering for his or her households’ nicely being. Nevertheless it wasn’t the Lehman chapter and the Nice Recession that despatched me to the ER.

It was the concern of failure…. lengthy hours, strain (each exterior and self-induced) and the office Machiavellian politics of the kind A bubble I used to be residing in that bought me there.

I noticed early on that the long-term prospects of me surviving, not to mention being pleased, in that setting weren’t good. However I didn’t but know what to do about it. And that definitely didn’t assist my anxiousness…

Is FIRE An Escape?

After which I heard about FIRE and the protected withdrawal charge. Impulsively, I had this magical perform of three numbers: internet value, expense finances, and 4%. This might free me of the rat race I used to be descending into.

If I might get my annual bills to be lower than 4% of my internet value, i.e. a moderately “protected withdrawal charge,” there was a really excessive likelihood that my belongings might cowl my bills via appreciation and varied types of revenue technology indefinitely.

For instance, let’s say my annual bills had been $40k and my internet value consisted of a broad inventory portfolio value $1M with none money owed. The expansion of that portfolio, monetized by way of dividends and inventory gross sales, might cowl my bills for the remainder of my life! I might be free to discover my passions and pursuits with out worrying a few paycheck.

FIRE Mindset and Values

I used to be about 6 or 7 years out of faculty at that time. However I had just a few issues working for me that aligned with a number of the primary tenets of FIRE, like a considerate, value-driven method to consumption and maximizing saving charge.

I had a poverty mindset that got here from rising up as an immigrant on welfare and public help. I noticed my single mom free us of that inside just a few years of arriving within the US. She utilized an unbreakable work ethic as she transitioned from being a civil engineer to performing probably the most primary duties at a nursing dwelling and cleansing homes as a “aspect hustle”.

I additionally had my highschool sweetheart, now my spouse, by my aspect. Having somebody supportive and aligned on the journey with you definitely makes it much more enjoyable. Sharing funds with one other individual as a part of a two revenue family for my whole grownup life made a big impact.

Getting Our Monetary Home in Order

I used to be capable of fairly shortly advance in my profession on Wall Avenue at a time the place compensation turned bipolar. The banks had been reducing senior workers (highest earners) and investing in retaining junior folks like me.

My spouse and I had been capable of go away faculty with little or no debt because of beneficiant, needs-based monetary support packages and dealing all through faculty. Fully paying that off was nonetheless the very first thing that we prioritized financially as soon as we graduated.

We additionally determined that we didn’t wish to have youngsters. Whereas that wasn’t a monetary resolution, it definitely helped construct our financial savings till we modified our minds once we had been almost in our mid 30s.

Because of this, we had been greater than midway to hitting our numbers the primary time I crunched them. I shared this magical discovery with my girlfriend (now spouse) and she or he agreed that this was the trail for us. We made a plan, set a goal date, and bought severe about making it occur.

Accelerating Our FIRE Plans

The plan advanced and dates moved over time, however we had been very lucky to have been capable of get there. I retired at 35 on Labor Day 2020. It was a little bit sooner than anticipated, however some occasions in my private life pushed me to make the leap. My spouse simply submitted her resignation and is at present figuring out her transition plan to be retired by the tip of the 12 months.

In some ways, FIRE was the end result of the American Dream for me. And I’ve been questioning whether or not that was nonetheless attainable for the technology simply getting began of their careers or for folks beginning to save later in life.

Associated: Do You Want Good Luck to Obtain Monetary Independence?

Getting Began

So, let’s dig in. Being a finance man, I like numbers. However I additionally like breaking issues down into simple to eat chunks. As I see it, there are three preliminary steps for anybody getting began:

- Create a finances on your retired life.

- Decide the required internet value to help that finances (ie construct your investments to not less than twenty-five occasions your annual spending akin to the 4% protected withdrawal charge).

- Create an funding plan to build up the required belongings to provide the revenue wanted to help that finances.

The very first thing you wish to do is get some ballpark estimates. Perceive the feasibility and normal form of your recreation plan.

Defining the Aim

Now, there may be an countless quantity of content material on the market about all of the nuances and issues of the above three steps. So I’m going to oversimplify issues on objective. Let’s simply take a look at the eventualities the place somebody units a retirement finances of $50K (“frugal”), $100K (“comfy”) and $300K (“luxurious”, aka FatFIRE).

Primarily based on the normal protected withdrawal charge of 4%, one would want to build up a internet value of $1.25M, $2.5M and $7.5M to help these budgets, respectively.

The second key axis to your internet value goal is the retirement age. The “normal” retirement age within the US is 64, in response to SoFi Be taught, which is a little bit over 40 years of working. So retiring after 30-35 years is sweet. Retiring after 10-15 is wonderful! I take advantage of 20 years as my baseline.

Figuring out Your Required Price of Return

The final piece you want for the again of the envelope calculation is the speed of return that you simply count on out of your earnings. I’m this from the angle of the latest faculty grad simply getting began.

That is typically an space the place the extra aggressive model investments can be beneficial. The commonest allocation can be a 100% broad-based, fairness portfolio. For instance, the Vanguard Whole Inventory Market ETF (VTI) is a very fashionable, low-cost funding product .

US fairness returns during the last 100 years have averaged round 10%. Nevertheless, most up-to-date, forward-looking forecasts put fairness returns someplace round an annualized 6% over the subsequent ten years. It is because we’re nonetheless close to the highest of an funding cycle. There’s a significant chance of recession over the subsequent few years. So to be a little bit conservative, I used 6% as my baseline.

That is the place an excellent retirement calculator turns out to be useful. However I simply did this in a spreadsheet. I like being fingers on with some of these issues to know the completely different dimensions once I’m doing one thing for the primary time.

Required Financial savings

Primarily based on my calculations, if your required finances in retirement is $50K, you would want to avoid wasting $50K per 12 months for 16 years to construct the required portfolio value $1.25M (assuming 100% fairness allocation averaging 6% annual return). Successfully, you could save your required retirement finances every year for 16 years

Alternatively you can save $34K per 12 months for 20 years. This might require saving 68% of your required finances every year to succeed in your purpose.

These numbers develop linearly for the opposite instances. You’d want to avoid wasting $100K yearly for 16 years or $68K for 20 years to succeed in a portfolio worth of $2.5M.

Observe the mathematics is basically the identical for an older saver who’s simply beginning to save for retirement.

Associated: 7 Advanatages When You Begin Saving for Retirement Late

It’s also value noting that taxes will not be linear and do introduce a little bit of complexity. An essential subsequent step after getting the essential image is to have a look at actual (i.e. accounting for inflation), after-tax revenue, returns and bills.

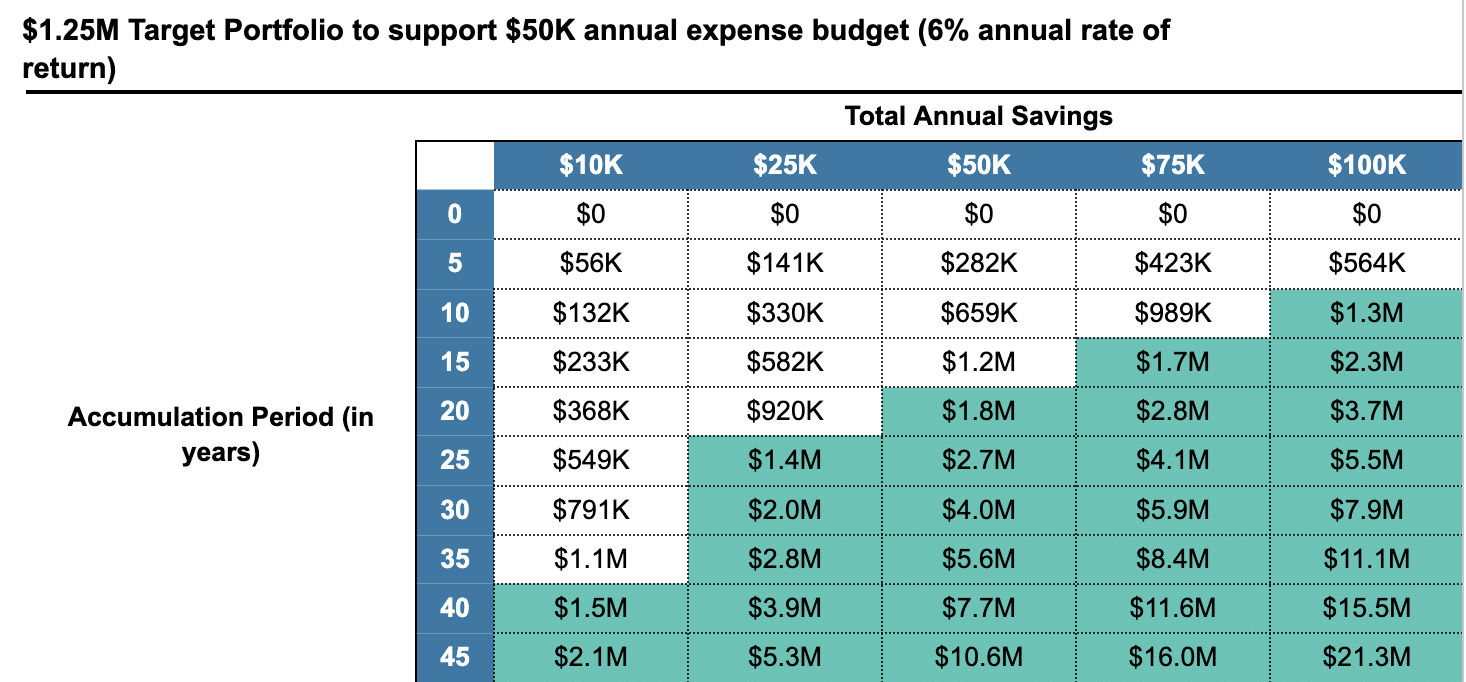

Under is a matrix that reveals completely different combos of financial savings per 12 months versus variety of years of accumulation. Areas in inexperienced is the place you attain your $1.25M goal. This helps a $50K finances on the conventional 4% withdrawal charge.

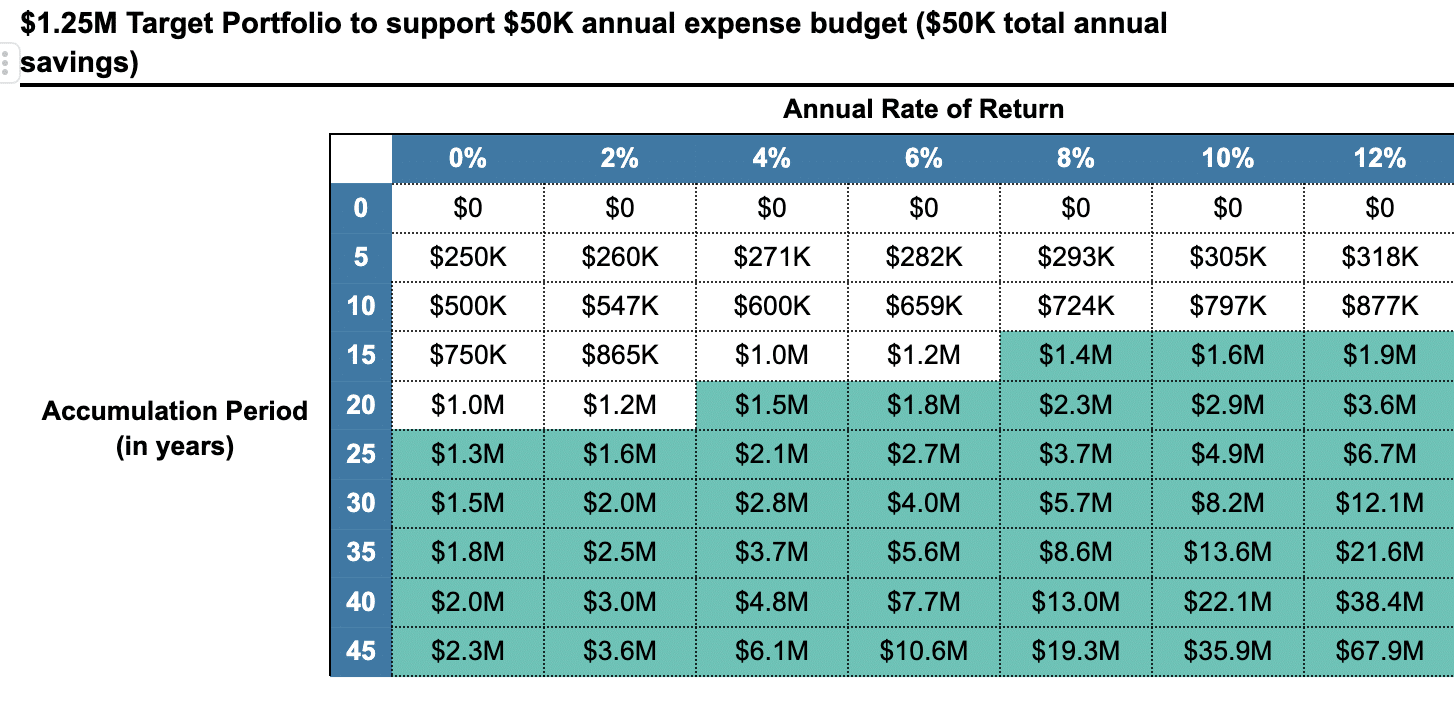

Right here is matrix to know how issues may be completely different over your 20 12 months accumulation interval relying on precise charges of return:

Is This Truly Potential As we speak?

To return to our beginning query – how possible is it for somebody simply getting began to efficiently save sufficient to retire early?

Headwinds

There are definitely quite a few headwinds.

- The everyday faculty graduate, as of 2022, is beginning almost $30K within the gap resulting from faculty loans. Common wage for that faculty graduate is just below $60K. Inflation has pushed the price of on a regular basis items up by almost 20% simply since Jan 2020.

- Common lease for a one bed room residence is $1,300 per thirty days (or $16K per 12 months). That varies from $730 in West Virginia to $1,650 in Hawaii. There’s a large quantity of variability with this knowledge between authorities (e.g. Census) and personal (e.g. Zillow) estimates. Non-public estimates recommend these numbers are even greater.

As with every little thing, there may be a lot variability within the calculation of the everyday value of residing. The typical annual bills for a latest faculty graduate appear to fall someplace between $35-$60K. So one would want $69-$94K in after-tax earnings, on common, to avoid wasting sufficient in 20 years for a $50K early retirement finances. That goes as much as $103-128K for the $100K early retirement finances.

Tailwinds

There are some tailwinds to contemplate as nicely.

- Advances in know-how and funding price compression have made it far simpler and cheaper to take a position right now than ever earlier than. You are able to do all of it with just a few faucets in your smartphone or have every little thing totally automated for you.

- Know-how can also be unlocking an ever-growing variety of revenue alternatives. What was as soon as relegated to the realms of “aspect hustles” is surpassing conventional employment revenue for many individuals. That is very true amongst youthful generations.

- Continued transfer to a service-based financial system, among the many different components talked about above, is making part-time and contract-based work extra prevalent.

- Covid has given everybody a brand new perspective on what’s essential. It has made folks extra value-driven of their selections and the worth calculation has change into much more holistic. It has additionally proven how resilient humanity may be within the face of unprecedented challenges.

The Actuality of “Early Retirement”

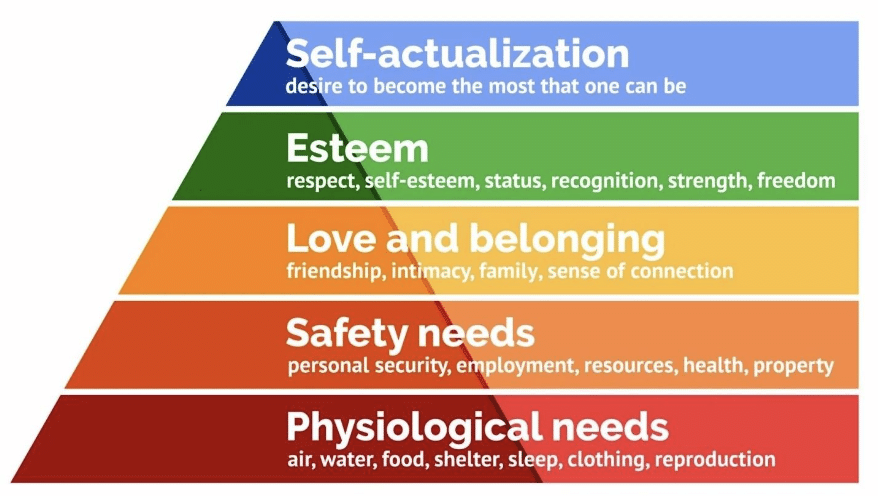

The truth is that with most early retirement, you will want to seek out different pursuits or pursuits to realize what Maslow put on the high of his hierarchy of human wants: Esteem and Self-Actualization.

The altering work dynamics are making it extra probably that assembly these wants in early retirement can produce some monetary revenue to complement your financial savings. For a lot of, early retirement turns into a interval of rewirement towards a extra genuine self reasonably than the “conventional” retirement.

Rules vs. Strategies

Whereas many essential features have definitely modified lately, it seems that a lot of the basic construction that determines whether or not or not you attain early retirement stays in place.

As at all times, having a excessive revenue goes to be among the many easiest paths to early retirement. For others, it’s going to in the end come right down to particular person selections.

Some folks may name them sacrifices. I want to consider them as priorities. What’s essential to you? What offers you pleasure? What has worth for you and the place does early retirement match into that?

You’ve the three most important dimensions to work inside:

- How a lot you spend (now and in retirement),

- Your saving charge (in share phrases and absolute {dollars} that your revenue permits), and

- The return you’re capable of get in your financial savings.

All of these have distinctive trade-offs and challenges.

Regardless of it feeling magical once I first realized about it, there’s actually no magic behind it. Chances are you’ll not be capable of predict all of the issues that the world will throw at you alongside the best way. And you might not have as a lot assist as others do.

However with a transparent plan guiding your selections and persistence in following the tried and true ideas, the highway to monetary independence and early retirement stays open to people who search to pursue it.

The place are you in your journey to early retirement? How do these numbers examine to your expertise? Do you assume you are able to do it for those who needed to begin from zero right now?

* * *

Precious Assets

- The Finest Retirement Calculators may also help you carry out detailed retirement simulations together with modeling withdrawal methods, federal and state revenue taxes, healthcare bills, and extra. Can I Retire But? companions with two of the very best.

- Free Journey or Money Again with bank card rewards and join bonuses.

- Monitor Your Funding Portfolio

- Join a free Private Capital account to realize entry to trace your asset allocation, funding efficiency, particular person account balances, internet value, money movement, and funding bills.

- Our Books

* * *

[Chris Mamula used principles of traditional retirement planning, combined with creative lifestyle design, to retire from a career as a physical therapist at age 41. After poor experiences with the financial industry early in his professional life, he educated himself on investing and tax planning. After achieving financial independence, Chris began writing about wealth building, DIY investing, financial planning, early retirement, and lifestyle design at Can I Retire Yet? He is also the primary author of the book Choose FI: Your Blueprint to Financial Independence. Chris also does financial planning with individuals and couples at Abundo Wealth, a low-cost, advice-only financial planning firm with the mission of making quality financial advice available to populations for whom it was previously inaccessible. Chris has been featured on MarketWatch, Morningstar, U.S. News & World Report, and Business Insider. He has spoken at events including the Bogleheads and the American Institute of Certified Public Accountants annual conferences. Blog inquiries can be sent to chris@caniretireyet.com. Financial planning inquiries can be sent to chris@abundowealth.com]

* * *

Disclosure: Can I Retire But? has partnered with CardRatings for our protection of bank card merchandise. Can I Retire But? and CardRatings might obtain a fee from card issuers. Different hyperlinks on this website, just like the Amazon, NewRetirement, Pralana, and Private Capital hyperlinks are additionally affiliate hyperlinks. As an affiliate we earn from qualifying purchases. If you happen to click on on one in all these hyperlinks and purchase from the affiliated firm, then we obtain some compensation. The revenue helps to maintain this weblog going. Affiliate hyperlinks don’t improve your value, and we solely use them for services or products that we’re accustomed to and that we really feel might ship worth to you. Against this, now we have restricted management over a lot of the show adverts on this website. Although we do try to dam objectionable content material. Purchaser beware.