{kind=link}

The temporary’s key findings are:

- Whereas annuities supply retirees assured lifetime earnings, few individuals have them.

- A brand new survey requested monetary professionals concerning the worth of annuities for his or her purchasers.

- The outcomes counsel that monetary professionals are involved that a lot of their purchasers may deplete their financial savings too shortly.

- However the majority of them don’t suggest annuities to their purchasers and, once they do, many purchasers don’t take the recommendation.

- These findings level to each the promise and limitations of reliance on monetary professionals to information purchasers to better use of annuities.

Introduction

The speed of possession of annuities in the USA is low, with solely about 10 % of older People having a business annuity. Researchers have provided many potential rationales as to why individuals approaching retirement have so little curiosity in annuities. Nevertheless, a largely ignored difficulty is how monetary professionals view annuities and the way their suggestions could have an effect on the acquisition of annuities amongst their purchasers.

This temporary, which is predicated on a latest survey, investigates how monetary professionals understand longevity threat and the worth of annuities for his or her purchasers. The findings counsel that the majority monetary professionals are conscious that a few of their purchasers could outlive their assets. However, the overwhelming majority of execs hardly ever suggest shopping for an annuity. Therefore, monetary professionals are at present doing little to encourage individuals approaching retirement to buy annuities.

The dialogue proceeds as follows. The primary part offers some background. The second part describes the survey. The third part presents the findings. The fourth part discusses their implications. The ultimate part concludes that monetary professionals are involved about their purchasers’ longevity threat and could also be a supply of untapped potential to extend annuity take-up.

Background

The small marketplace for non-public sector annuities in the USA has confounded lecturers and policymakers for many years. Quite a few hypotheses for the low demand have been superior, all revolving across the many causes that people could not need to annuitize. Nevertheless, latest work means that many people would purchase an annuity if the method have been easy, however are prevented from doing so by the real-world complexity of the duty.

A lot of that complexity entails a sequence of small hurdles, which collectively may stymie even a motivated potential annuity purchaser. For instance, realizing a product like an annuity even exists shouldn’t be trivial. Survey proof means that even amongst comparatively rich households (over $100,000 in monetary property) close to or in retirement, greater than a 3rd weren’t conversant in lifetime earnings merchandise, and one other 40 % have been solely considerably acquainted. These estimates in all probability overstate familiarity for the inhabitants as a complete, since respondents typically dislike admitting ignorance, and these wealthier respondents usually tend to be acquainted with annuities than their much less prosperous counterparts.

Monetary professionals may assist by explaining what annuities are, who sells them, the best way to contact suppliers, and the best way to put together for really signing a contract. All these steps may get people who want no convincing to easily take the concrete steps between a need for lifetime earnings and really buying it. The latest survey means that about half the inhabitants with over $100,000 in monetary property wish to purchase a lifetime earnings product on the prevailing worth. Moreover, professionals may clarify the worth of annuities to these with lower than $100,000 in property who may be on the fence. The query is: do professionals do any of these items?

The Survey

The survey, carried out by Greenwald Analysis in June of 2023, questioned 400 monetary professionals concerning the matters they focus on with their purchasers and the suggestions they make. It additionally requested them a number of questions on their purchasers’ longevity, whether or not they suggest annuities, what sort of annuities they’re most certainly to suggest, and whether or not their purchasers comply with their recommendation.

Monetary professionals have been chosen based mostly on the next traits. First, they’d over $30 million underneath administration. Second, they’d greater than three years {of professional} expertise. Third, they made suggestions themselves to their purchasers. Fourth, over 50 % of their earnings got here from monetary planning, investments, life insurance coverage, and associated services and products with particular person purchasers, versus worker advantages or different group merchandise, medical health insurance, and property/casualty insurance coverage. Fifth, they’d greater than 75 purchasers.

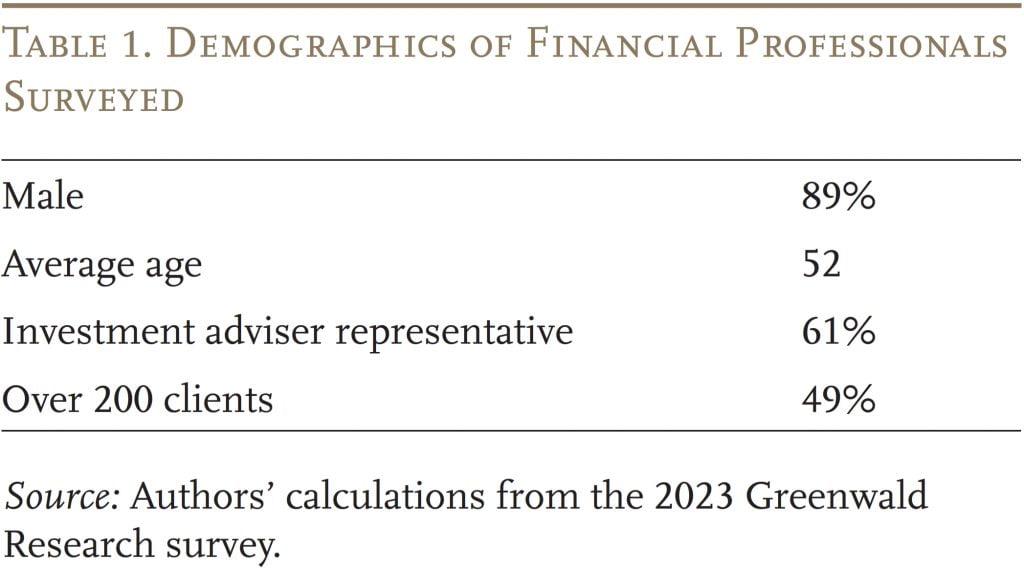

Desk 1 reveals the pattern’s abstract statistics. The skilled individuals are overwhelmingly male, and their common age is 52. Roughly half advise over 200 purchasers.

Outcomes

The survey means that monetary professionals know that their purchasers would possibly dwell to very previous ages and outlive their assets. Roughly 76 % of monetary professionals focus on the possibility of residing to superior previous age, similar to age 95, with their purchasers. Relating to longevity threat, the survey signifies that greater than 90 % of them are not less than considerably involved that their purchasers will deplete their financial savings.

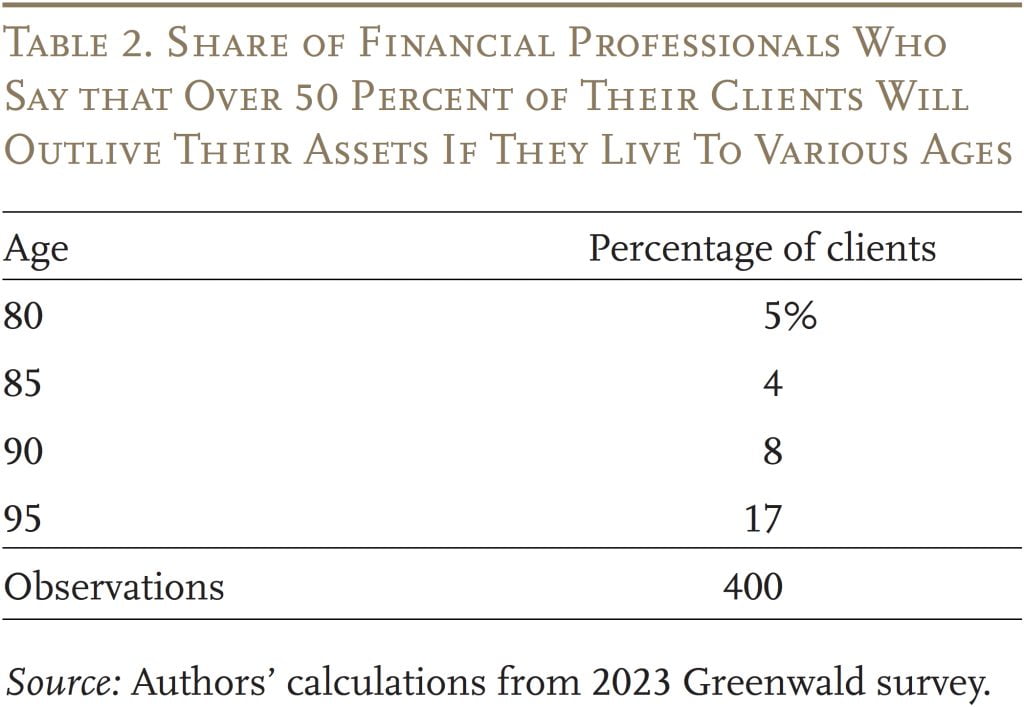

The survey additionally requested monetary professionals to estimate the share of their purchasers that may outlive their property in the event that they dwell to sure ages. The responses present that 17 % of monetary professionals imagine that greater than half of their purchasers will outlive their assets in the event that they dwell to age 95 (see Desk 2). In truth, nationwide about 10 % of purchasers will dwell to 95, and face the extreme penalties of exhausting their assets. Be aware, additional, that people who go to monetary professionals have considerably extra wealth than the typical American, which has offsetting implications. On the one hand, a better proportion will dwell to 95; however, their larger asset ranges can function a buffer.

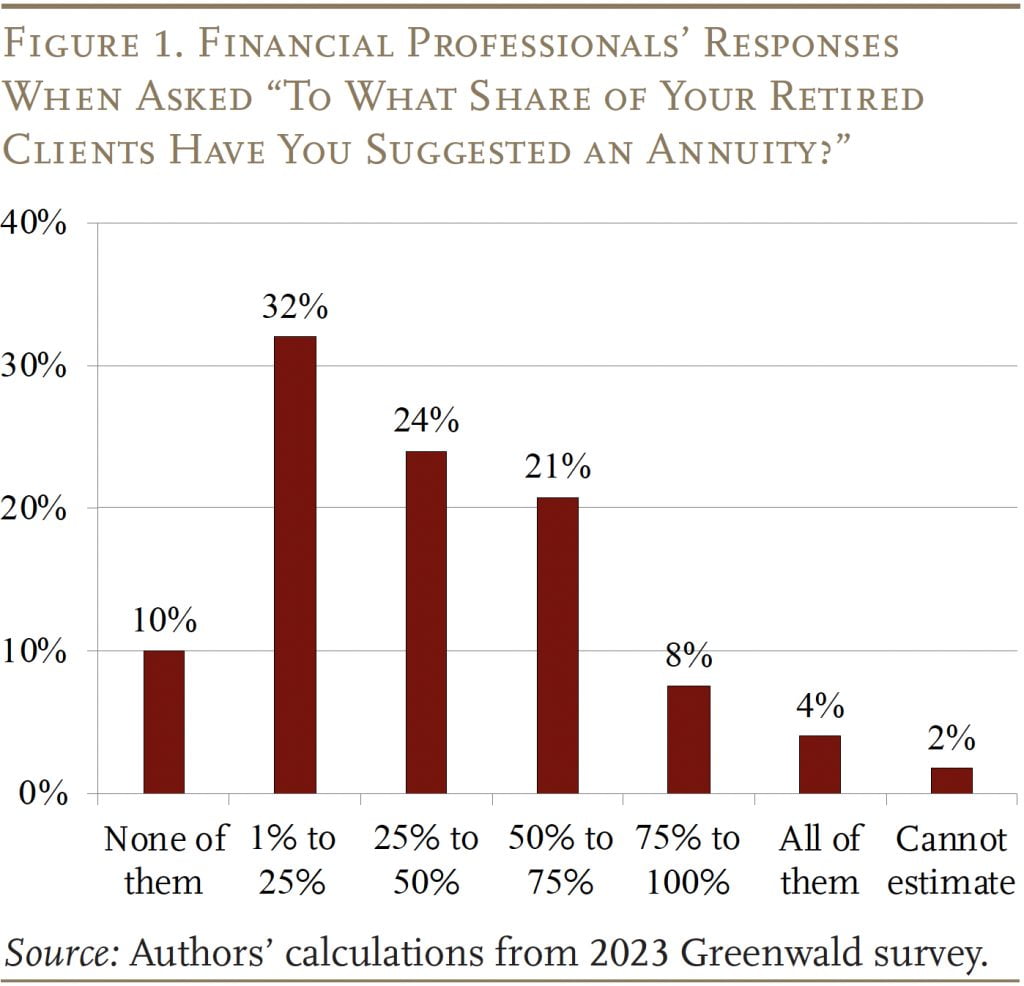

With respect to defending in opposition to longevity threat, the survey additionally requested the monetary professionals how typically they suggest shopping for an annuity. Determine 1 reveals that roughly two-thirds of execs suggest an annuity to lower than half of their purchasers. Greater than two-fifths suggest an annuity with assured lifetime earnings to lower than 1 / 4 of their purchasers.

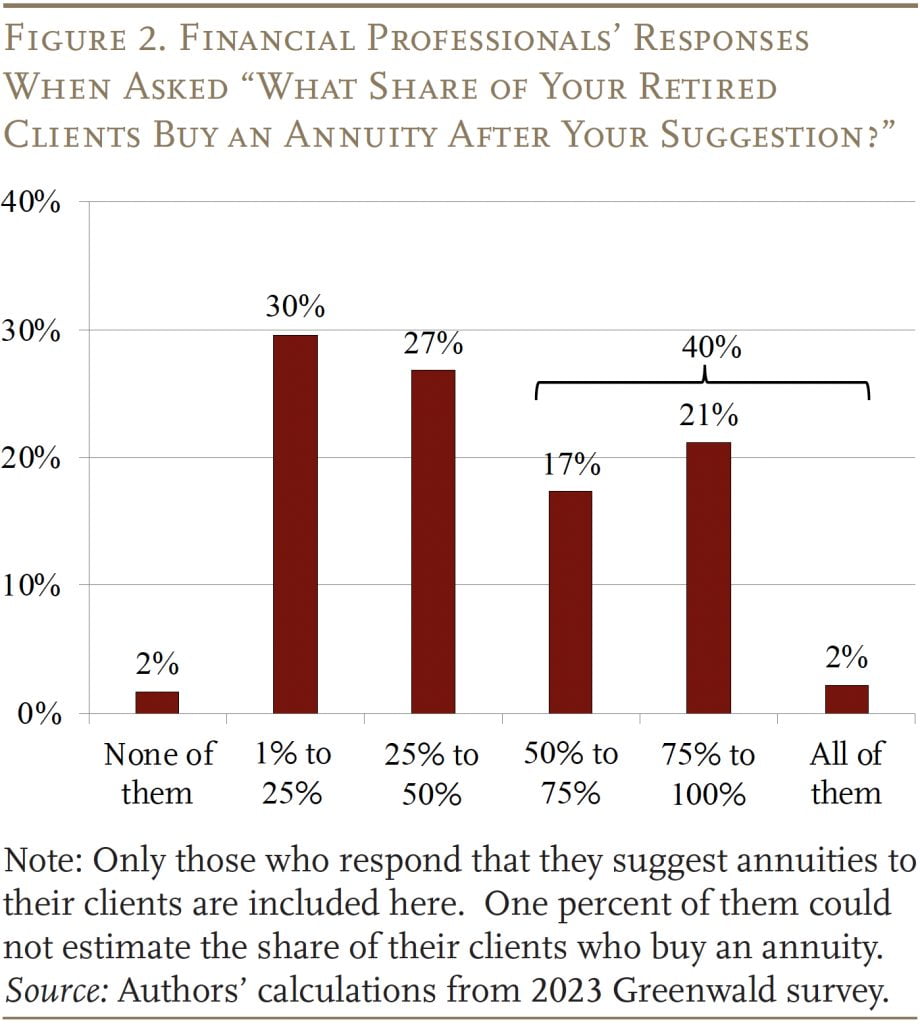

Lastly, when monetary professionals do counsel annuities, 40 % imagine that the majority of their purchasers comply with their ideas (see Determine 2).

Dialogue

The survey means that monetary professionals are conscious of their purchasers’ longevity threat and focus on this subject with them. Thus, the truth that most professionals don’t sometimes suggest any annuitization is stunning. A part of the rationale could also be that the majority of purchasers don’t are likely to comply with such recommendation when given.

Therefore, the survey factors to each the promise and the constraints of reliance on monetary professionals to information purchasers to better use of annuities with assured lifetime earnings. Professionals may very well be far more proactive in recommending annuitization. A considerable minority of purchasers would comply with such recommendation if it have been provided, notably if the recommendation have been accompanied by steering on the best way to go about buying an annuity.

Moreover, the outcomes from earlier analyses counsel that monetary professionals have untapped potential in rising annuity take-up. Since roughly half of those that can afford to annuitize (these with over $100,000 in monetary property) point out they might purchase an annuity if the method have been easy, professionals can play a job in facilitating such transactions to serve each their purchasers’ wants and their wishes.

Conclusion

The outcomes of the survey counsel that monetary professionals are deeply involved about a lot of their purchasers’ potential to handle longevity threat. However, the vast majority of monetary professionals don’t sometimes suggest annuity merchandise to their purchasers. Amongst those that do, many report that their purchasers don’t comply with their advice. This discovering means that monetary professionals appear to have the power to affect solely a modest portion of their purchasers.

The outcomes additionally level to areas for additional analysis: how ought to professionals establish which purchasers could be receptive to annuities? And would sure messaging approaches (e.g., saying “lifetime earnings” quite than naming a particular monetary product) work higher than others to persuade these purchasers who’re on the fence? General, nevertheless, the lowest-hanging fruit is probably going serving to the purchasers who already are open to annuities obtain their present lifetime earnings objectives.

References

Arapakis, Karolos and Gal Wettstein. 2023a. “Longevity Danger: An Essay.” Particular Report. Chestnut Hill, MA: Middle for Retirement Analysis at Boston School.

Arapakis, Karolos and Gal Wettstein. 2023b. “How A lot Do Folks Worth Annuities and Their Added Options?” Working Paper 2023-18. Chestnut Hill, MA: Middle for Retirement Analysis at Boston School.