Older high-income households with a 401(okay) gained; everyone else misplaced.

The Federal Reserve’s 2022 Survey of Client Funds (SCF) summarizes modifications in household funds between 2019 and 2022 – three years of COVID and financial disruption, and 2022 was additionally a horrible yr when it comes to inventory and bond returns. On the similar time, the federal government offered unprecedented fiscal assist, employment remained sturdy, the inventory market – even with the drop in 2022 – ended up considerably greater than in 2019, and the 401(okay) system continued to mature. On stability, one would anticipate improved retirement balances between 2019 and 2022 throughout age and revenue teams.

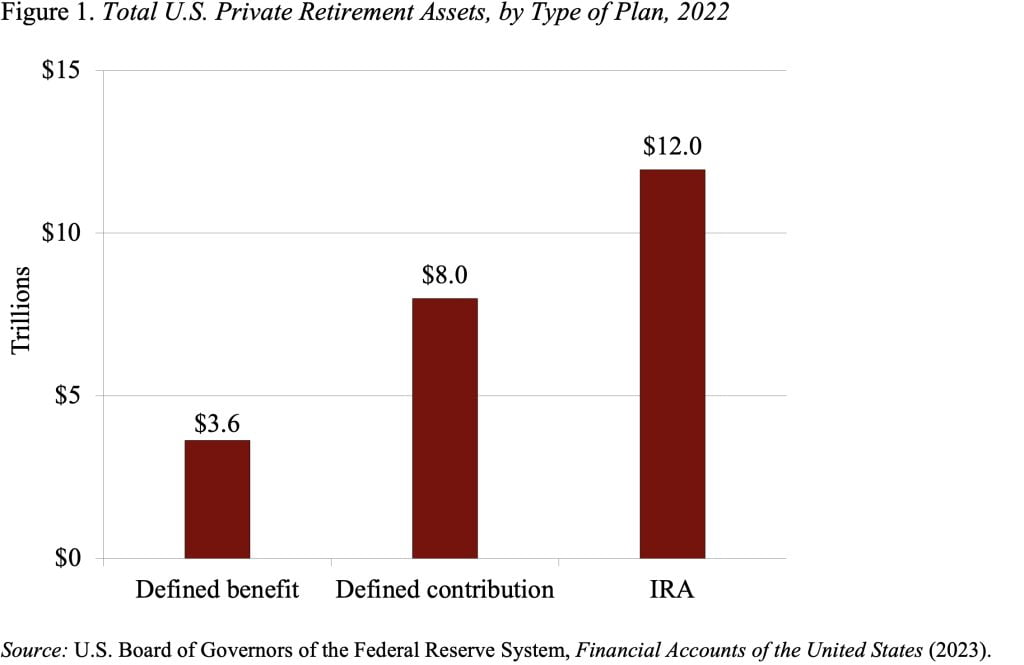

The benefit of the SCF over information on 401(okay) plans from monetary service companies is that it supplies data not solely about households’ 401(okay) holdings but additionally about their IRAs, that are predominately rollovers from 401(okay)s and signify nearly all of retirement account property (see Determine 1).

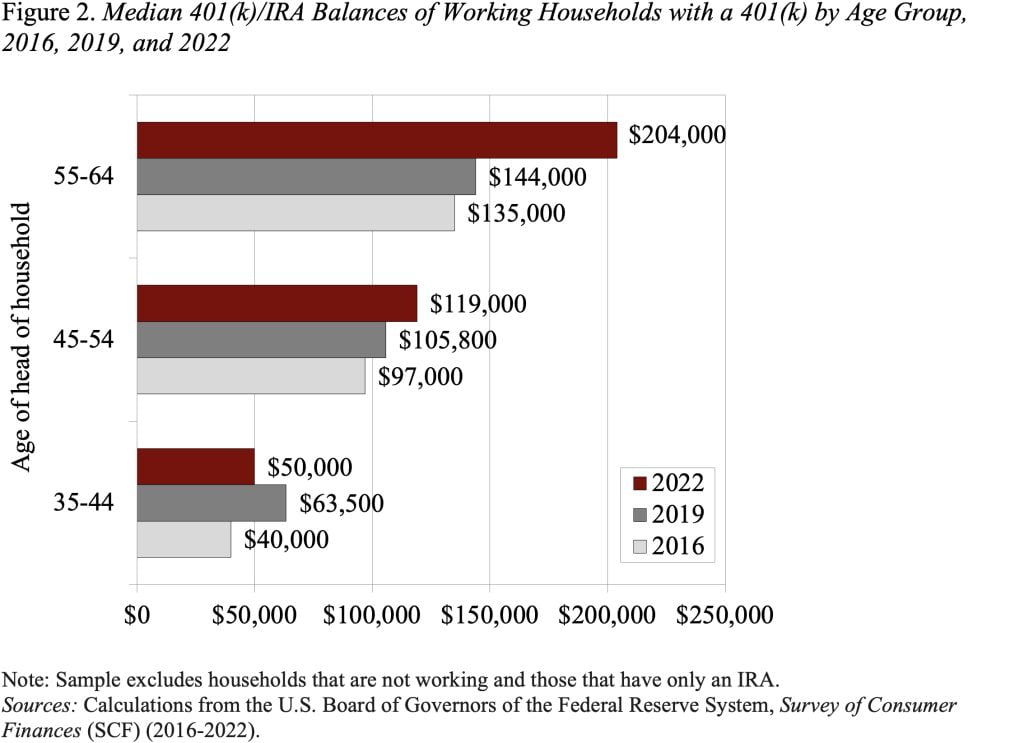

The excellent news from the 2022 SCF is that 401(okay)/IRA balances for older working households with a plan totaled $204,000 in 2022 in comparison with $144,000 for comparable households in 2019. (see Determine 2). The information for youthful households, nonetheless, is much less rosy. The median 401(okay)/IRA balances for households ages 45-54 elevated solely from $105,800 to $119,000 – lower than the speed of inflation. And the holdings of the youngest group (35-44) really declined.

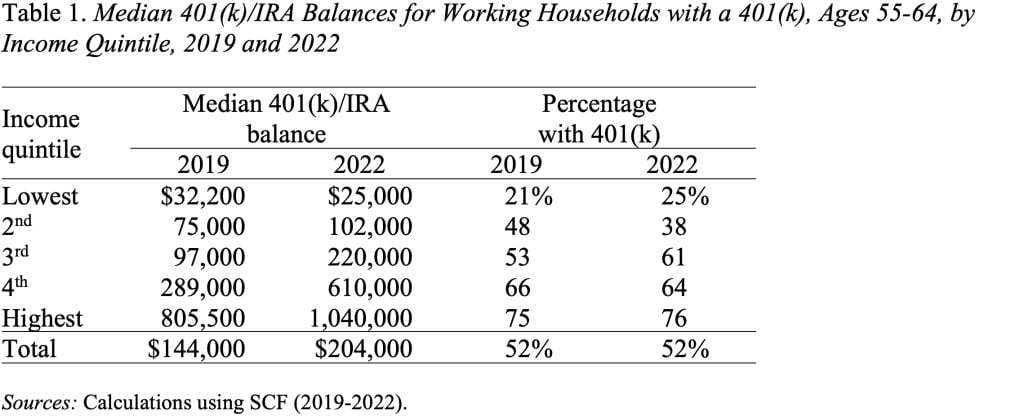

Furthermore, the beneficial properties in 401(okay)/IRA balances weren’t unfold evenly throughout the revenue distribution of working households. The center quintile gained not solely in balances but additionally within the proportion of households with a 401(okay) plan. That’s clearly excellent news. Larger-income households noticed even bigger proportion will increase of their balances, and the share of households with a plan held regular. For the underside two quintiles, the information will not be good. Both balances dropped or balances elevated however the proportion with a plan dropped sharply (see Desk 1).

On stability, given the power of the economic system and the beneficial properties within the inventory market over the three-year interval, the 2022 SCF supplies a disappointing image of the retirement property for working households. Furthermore, the main target is on the 50 p.c of households with a 401(okay) plan; the opposite half of households don’t have anything however Social Safety. Clearly, making certain the solvency of Social Safety is a excessive precedence.

The Entrepreneurial Mindset: Traits to Construct Success

The Entrepreneurial Mindset: Traits to Construct Success{kind=link}