{kind=link}

Regardless of intensive modifications to the Nationwide Retirement Threat Index’s platform, methodology, and information, the image stays the identical.

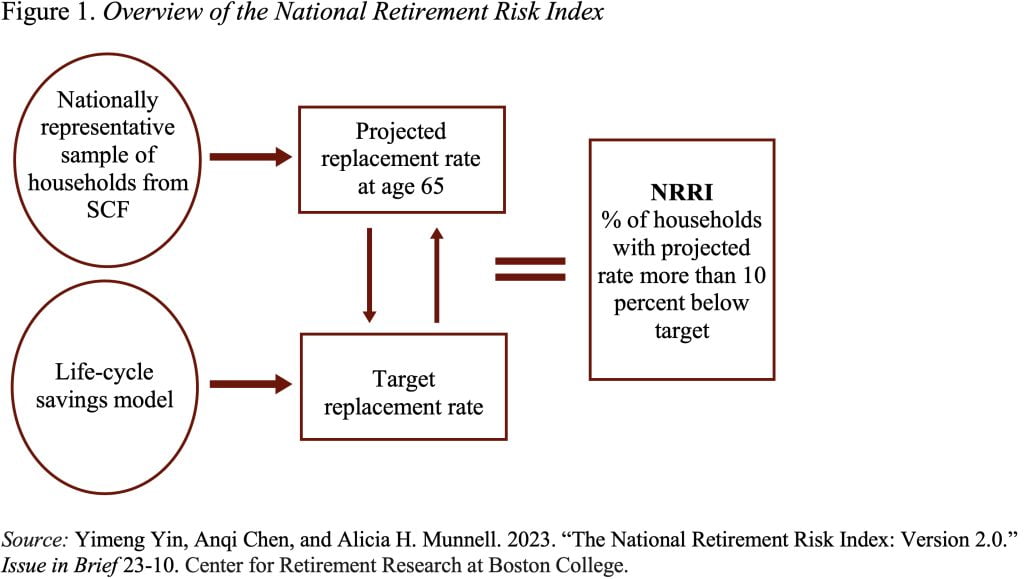

The Heart first launched its Nationwide Retirement Threat Index (NRRI) in 2006. The aim was to summarize in a single quantity the extent to which as we speak’s staff can be ready for retirement. The Index makes use of the Federal Reserve’s triennial Survey of Client Funds to match projected substitute charges – retirement revenue as a share of pre-retirement revenue – with goal charges that will enable households to take care of their dwelling normal. These households with a projected substitute fee that’s greater than 10 p.c beneath the goal are characterised as falling quick (see Determine 1).

After almost twenty years of updating information and modifying this system, the index was sorely in want of unpolluted up. Candidly, its innards had been a multitude. My colleague Yimeng Yin labored on the mission solidly for 9 months. Along with updating information and shifting the codebase from Stata and Excel spreadsheets to Python, we selected 4 main enhancements:

- Shifting the premise for projecting wealth-to-income from means to medians, which makes the wealth projections at retirement higher replicate the noticed distributions.

- Projecting monetary property and non-mortgage debt individually, permitting for extra in-depth evaluation in addition to counterfactual evaluation specializing in borrowing.

- Utilizing a lot richer family traits for calculating goal substitute charges.

- Incorporating the Earned Revenue Tax Credit score in substitute fee calculations to higher seize the revenue these households might want to substitute in retirement.

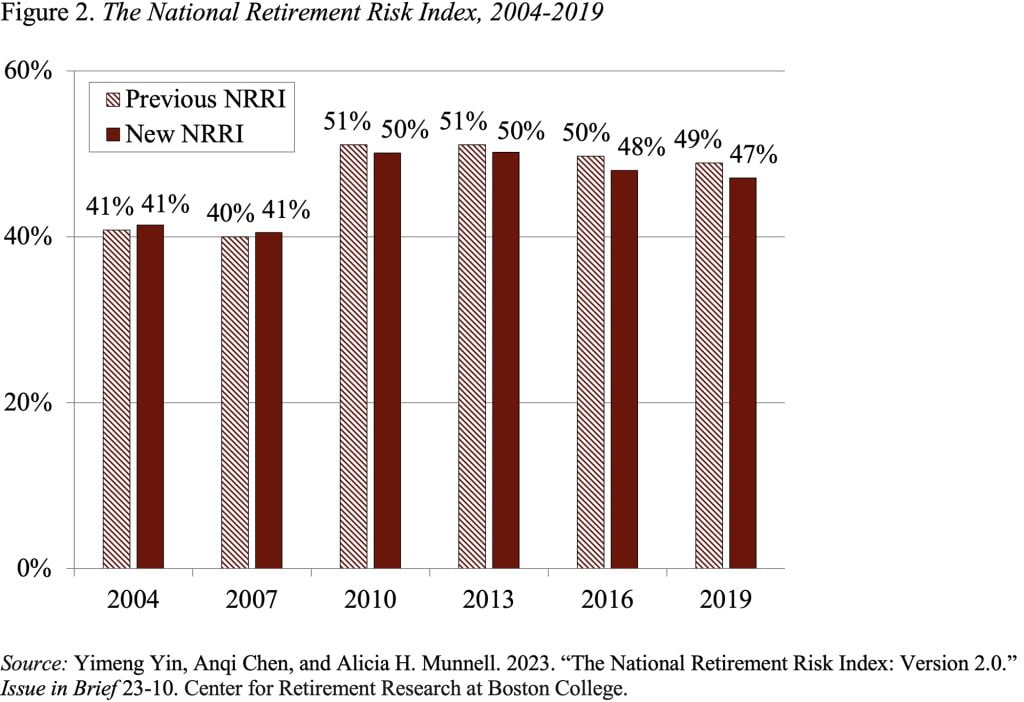

Regardless of the intensive modifications in information and methodology, the general stage and time sample of the Index stay the identical as earlier than (see Determine 2). Thus, a very powerful discovering nonetheless holds: about half of working-age households will be unable to take care of their pre-retirement dwelling normal.

Furthermore, the sample continues to replicate the well being of the economic system. The Index elevated considerably from 2007 to 2010 through the Nice Recession, after which declined a bit from 2013 to 2019 because the economic system loved low unemployment, rising wages, sturdy inventory market progress, and rising housing costs. These enhancements had been modest attributable to some countervailing longer-term traits – such because the gradual rise in Social Safety’s Full Retirement Age (FRA) and the continued decline of rates of interest – which made it harder for households to realize retirement readiness.

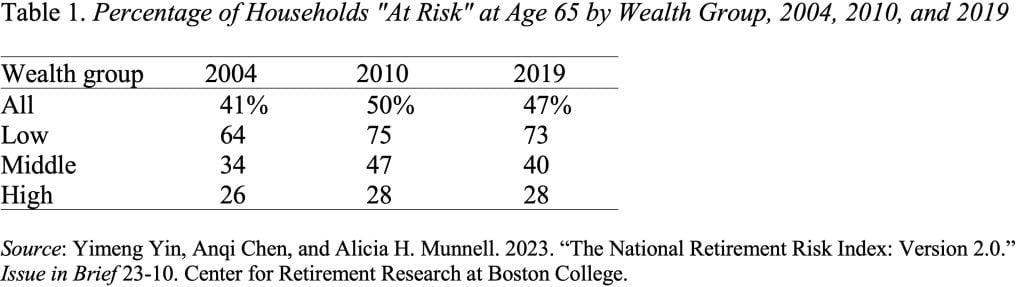

When seen by wealth, households’ retirement preparedness exhibits a smart sample, with a big distinction between the highest and backside wealth teams (see Desk 1).

The underside line is that – irrespective of how a lot the methodology is modified and the information up to date – the NRRI continues to indicate a big share of as we speak’s working-age households will be unable to take care of their pre-retirement lifestyle as soon as they retire. This isn’t a time to even ponder reducing again on Social Safety advantages. And it’s the time to push for common protection by retirement financial savings plans so that each family has some capability to avoid wasting extra cash.