{kind=link}

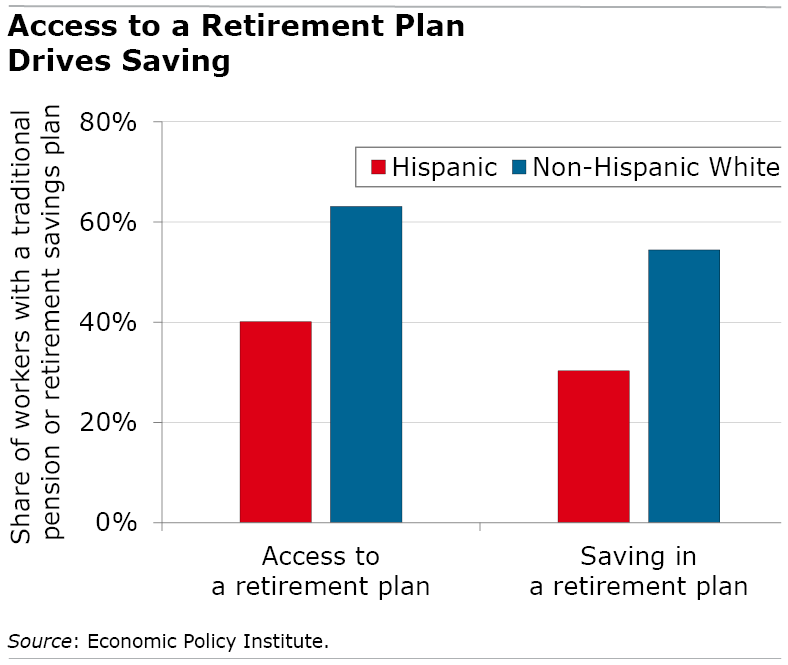

U.S. staff’ enthusiasm for saving cash for retirement is lukewarm. However that doesn’t go very far in explaining why solely three out of each 10 Latino staff are collaborating in an employer retirement plan, sometimes a 401(okay).

The main purpose is that the majority of them should not have a retirement plan as a result of they’re employed in low-wage blue-collar or service industries – roofing, dishwashing, meals preparation, landscaping, inns, maid and janitorial companies. These kind of jobs are sometimes crammed by latest or undocumented immigrants and don’t embrace any worker advantages.

The Financial Coverage Institute estimates that solely 4 out of 10 Latino staff have a retirement plan of their present jobs. In that mild, the majority of the people are benefiting from it, as a result of three out of the 4 Latinos who’ve entry to a plan are collaborating in a single.

Santiago Sueiro, senior coverage analyst at UnidosUS, a Latino advocacy group, stated the low numbers are solely a part of the image and don’t mirror how many individuals are saving. If undocumented staff corresponding to day laborers or housekeepers are being paid in money, they could be saving cash in money. Many individuals additionally ship a reimbursement to their house nation, the place they’re both shopping for or constructing a home outright that they will use after they retire and return house.

“Extra persons are saving informally than the information would counsel,” Sueiro stated. “Persons are attempting to make it work any approach they will,” and shopping for a home “is a culturally completely different approach of attempting to avoid wasting up for outdated age.”

However he additionally stated 401(okay)s have increased returns, and he wish to see extra use within the Latino neighborhood. The widespread lack of retirement financial savings is a specific drawback, as a result of life expectancy amongst Latino women and men is increased than amongst non-Latino White women and men. This “predictably lead[s] to aggravated financial issues in outdated age,” one examine concluded.

However issues are additionally altering quick. Lots of the individuals who have been born right here – and that describes two-thirds of the nation’s Latinos and Hispanics – or who immigrated at a younger age have assimilated to U.S. tradition and are flourishing, stated Michael R. Acosta, proprietor of Genesis Wealth Planning in Charlotte, North Carolina, who’s growing a shopper base locally.

And they’re more and more going to school. The variety of Latinos with not less than a bachelor’s diploma has greater than doubled over the previous 15 years, far outpacing the inhabitants’s development. Analysis has proven that extra educated individuals, who normally earn extra, usually tend to have an employer retirement plan.

Nevertheless, there are large ethnic variations in faculty attendance. Folks of Cuban descent are among the many most probably to have a bachelor’s diploma, and so they are inclined to earn extra, based on a 2013 Pew examine. Folks of Mexican descent have one of many lowest charges of school levels and Puerto Ricans have among the many lowest incomes, each indications they’re within the sorts of jobs that don’t present a retirement plan.

Acosta stated his personal Colombian immigrant household’s expertise is an instance of the varied approaches to retirement in his neighborhood.

His mother and father immigrated after they have been kids. His father owned a reworking and portray firm and stored his financial savings in money, slightly than the inventory market, as monetary advisers like Acosta suggest. Building can be an up-and-down enterprise, and the monetary struggles throughout the gradual seasons made it troublesome for his father to construct up a surplus of financial savings. This phenomenon is frequent within the self-employed building trade.

His mom, however, had an organization job with a 401(okay) that gave her the chance to organize for retirement. Acosta’s mother and father are divorced, and his mom is extra financially safe in her retirement due to that employer plan. The distinction between their monetary outcomes is “evening and day,” Acosta stated.

A number of of his aunts and uncles rely predominantly on Social Safety for retirement, which is quite common within the Latino neighborhood. Social Safety estimates that the packages’ retirement advantages present the overwhelming majority of revenue for about 40 p.c of married {couples} – double the speed for non- Latino Whites. And Social Safety is the first supply of revenue for 59 p.c of single Latino retirees – and in addition a lot increased than single non- Latino Whites.

However Acosta’s aunts and uncles are additionally examples of the follow of investing in actual property inside and outdoors of the USA as a type of saving. “They’re not collaborating [in a 401(k)], however they’re additionally doing okay,” he stated.

One aunt, who’s single and primarily labored in textile mills, now not has a mortgage on the home she’s lived in for some 25 years. As a result of she has such a low value of dwelling, “Social Safety goes to cowl most of her primary wants,” Acosta stated. Different family have invested in rental properties in South America that present a dependable supply of retirement revenue.

One other situation is latest immigrants’ hesitancy about investing or utilizing conventional monetary establishments. “There’s a scarcity of belief and monetary literacy,” he stated.

Latinos on this nation come from myriad cultures, and there are large variations of their experiences, immigration standing, and socioeconomic positions. Their retirement conditions are equally various.

Squared Away author Kim Blanton invitations you to comply with us on Twitter @SquaredAwayBC. To remain present on our weblog, please be part of our free e-mail listing. You’ll obtain only one e-mail every week – with hyperlinks to the 2 new posts for that week – while you join right here. This weblog is supported by the Middle for Retirement Analysis at Boston Faculty.