{kind=link}

Now that COVID is fading, researchers wanting again on the monetary help handed by Congress in the course of the pandemic are concluding that it helped hundreds of thousands of Individuals get by means of a time of unprecedented misery.

That the help can be satisfactory was not apparent within the midst of the financial turmoil in 2020 as COVID unfolded. However a 12 months into the pandemic, Individuals had been feeling higher off after the infusions of money from federal reduction checks and extra beneficiant advantages for laid-off staff that included an additional $600 per thirty days and – for folks with property – hovering home and inventory costs.

When working-age adults had been requested in 2021 how they perceived their funds, 36 p.c mentioned they’d have bother protecting a $400 expense in an emergency. Again in 2019 – earlier than the COVID help – 41 p.c felt that means.

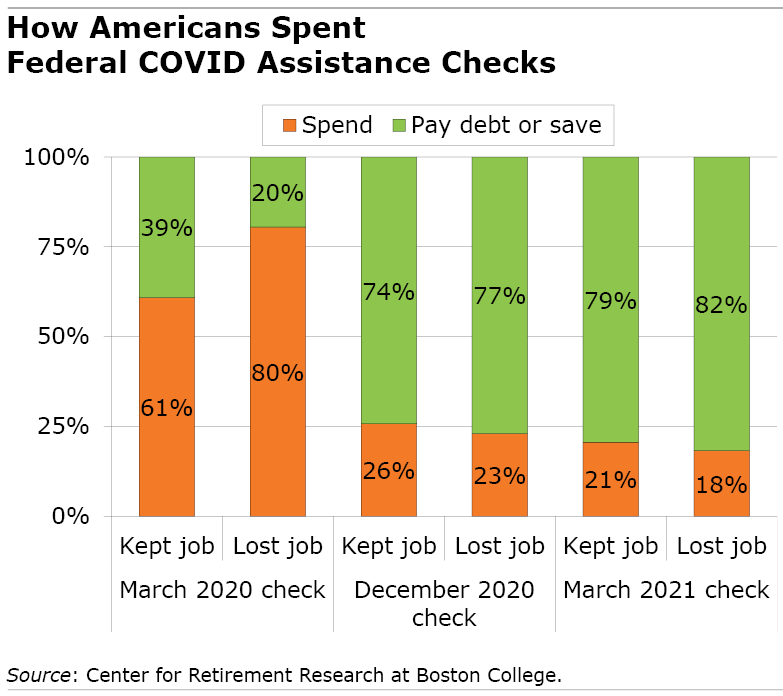

And though most individuals spent the primary checks the federal government issued in March 2020, the overwhelming majority felt snug depositing the 2 later checks within the financial institution or utilizing them to repay debt.

Perceptions that their funds had been holding their very own or enhancing, regardless of the pandemic, lined up pretty properly with actuality. However the dynamics had been very totally different for every of the three wealth teams – low, center and excessive – analyzed in a brand new research of modifications in U.S. households’ web price by the Heart for Retirement Analysis at Boston School.

The federal reduction was, for a lot of, a big infusion of money. For instance, married working {couples} incomes lower than $150,000 acquired as a lot as $6,400 in reduction checks and little one assist.

Nonetheless, people and households who entered the pandemic with low quantities of wealth or no wealth primarily broke even. And breaking even was a significantly better consequence than they’d skilled after the Nice Recession – and extra notable since they felt the brunt of the 2020 layoffs and misplaced revenue when unemployment soared to just about 15 p.c.

However administrative delays on the state stage clogged the pipeline of unemployment checks, inflicting delays in distributing the advantages. Congress’ approval of enhanced jobless advantages was additionally sporadic. And households spent extra on meals and housing, partly attributable to rising costs.

Amongst households with low wealth ranges, “the unfavorable affect of earnings losses from unhealthy labor market experiences and will increase in consumption totally offset the stimulus funds,” the research concluded.

Households with center and excessive ranges of wealth additionally went by means of layoffs and pay cuts when companies shut down, though to a lesser extent. They emerged from the worst of the pandemic with significantly extra wealth than after they went into it.

Center-wealth households elevated their web price by $38,700 in 2020 and 2021, because of rising asset costs and the federal help and advantages that went to individuals who’d misplaced their jobs. Excessive web price households’ wealth grew by $1.73 million over the 2 years, and the explanation boiled right down to surging inventory and home costs that beefed up their already-hefty portfolios. These positive aspects dwarfed the quantity of their reduction checks.

This research is a primary take a look at the affect on wealth of the federal government’s COVID help, and extra evaluation can be wanted to see whether or not the positive aspects final by means of 2023’s excessive inflation. However the excellent news is that Individuals apparently emerged from the turmoil in significantly better monetary form than after the Nice Recession.

To learn this analysis temporary by Andrew Biggs, Anqi Chen, and Alicia Munnell, see “How Did the Pandemic Have an effect on Family Steadiness Sheets?”

The analysis reported herein was derived in entire or partly from analysis actions carried out pursuant to a grant from the U.S. Social Safety Administration (SSA) funded as a part of the Retirement and Incapacity Analysis Consortium. The opinions and conclusions expressed are solely these of the authors and don’t signify the opinions or coverage of SSA, any company of the federal authorities, or Boston School. Neither america Authorities nor any company thereof, nor any of their staff, make any guarantee, specific or implied, or assumes any authorized legal responsibility or accountability for the accuracy, completeness, or usefulness of the contents of this report. Reference herein to any particular business product, course of or service by commerce identify, trademark, producer, or in any other case doesn’t essentially represent or suggest endorsement, suggestion or favoring by america Authorities or any company thereof.