{kind=link}

And what’s the outlook for Gen-Xers and Millennials?

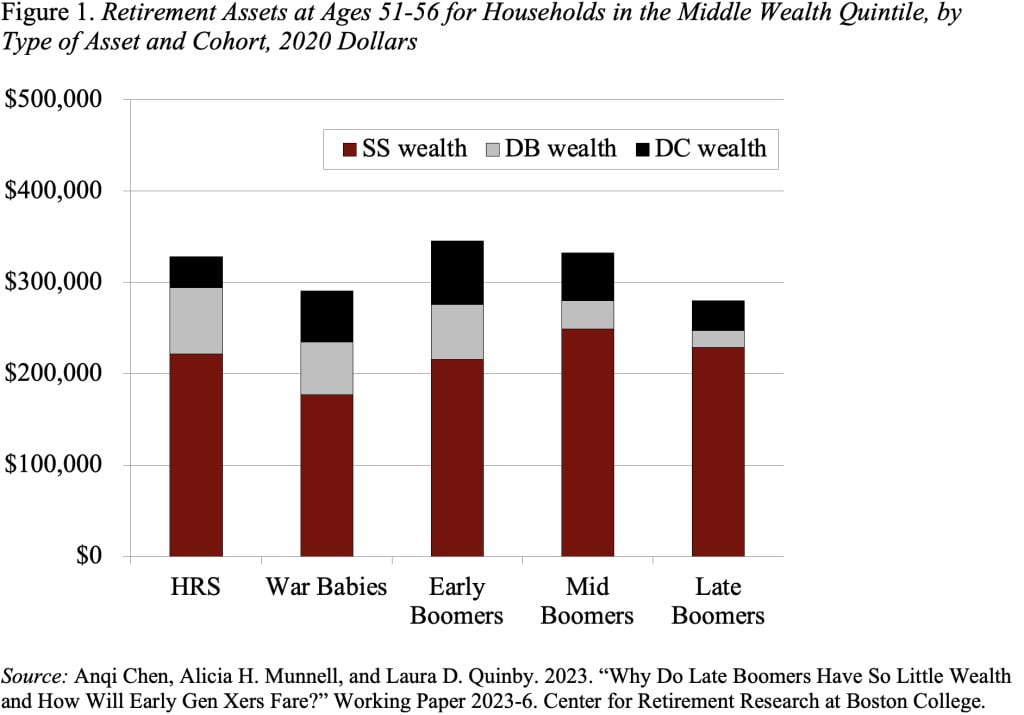

Late Boomers have low ranges of wealth no matter how it’s outlined – whole wealth, retirement wealth, or 401(okay)/IRA wealth. A decline in some wealth parts had been anticipated on account of the rise in Social Safety’s Full Retirement Age, the shift from outlined profit (DB) to outlined contribution (DC) plans, and a drop in housing values in the course of the Nice Recession. However rising DC balances had been predicted to offset the hole, since Late Boomers had been the primary technology the place employees may have spent their complete profession lined by a 401(okay) plan. That didn’t occur; common DC wealth for these within the center quintile dropped from $52,300 for Mid Boomers to $32,700 for Late Boomers (see Determine 1). In actual fact, declines occurred throughout all however the high quintile.

My colleagues and I’ve simply accomplished a examine to determine why Late Boomers have so little retirement wealth and what the patterns indicate for Early Gen-Xers and subsequent cohorts. We used a decomposition method that types out the contribution from varied sources. The findings indicated that two main elements had been at play – a change within the composition of households and a weakening for Late Boomers of the hyperlink between work and wealth accumulation.

This isn’t a story of the deteriorating standing of Black and Hispanic households; certainly, the wealth of non-White households has elevated relative to their White counterparts. However Black and Hispanic households nonetheless have much less wealth than White households, so after they enhance as a share of the whole households, common cohort wealth will decline. Equally, a decline within the proportion of households married or with a school diploma will carry down the typical. For whole wealth and retirement wealth, the altering demographics accounted for 24-29 % of the whole decline.

The remaining was attributable to shifting coefficients – crucial of which was the weakened hyperlink between work and wealth. This sample is absolutely in keeping with knowledge from different surveys which present Late Boomers, who had been of their 40s on the time, had been hit exhausting by the Nice Recession and by no means recovered. Even Late Boomers who had a job after the Nice Recession earned much less, had been much less more likely to take part in a 401(okay) plan, and accrued fewer property in these plans. Work, for Late Boomers, merely didn’t produce the enhance to wealth accumulation that it had for earlier cohorts.

This discovering is doubtlessly excellent news for the wealth holdings of future generations. Whereas the demographic/training shifts will proceed to carry down the typical, these elements weren’t the foremost supply of the decline. The large change was the weakening of the hyperlink between work and wealth accumulation for the Late Boomers on account of the Nice Recession. To the extent that the decline in wealth is a Nice Recession story, a few of the downward strain on wealth holdings ought to abate.

Let’s hope we’re proper!